My last post was on credit cards, why you should get one, and how to not suck at using them. Working down the list of things-I’ve-learned-about-and-feel-comfortable-talking-about and not the list of actually-important-things-to-do-in-order, I wanted to write about high yield savings accounts (HYSAs), which serve as a place to park things like emergency funds or savings for near-term large purchases.

A Bit of Motivation: Free Money?

Last time, I talked about how credit cards were “free money” and then some, due to the rewards and perks you can get from using them responsibly (again, always pay off the full balance each month). HYSAs aren’t really “free money” per se due to inflation (which I’ll touch on later), but they’re much better than standard savings accounts.

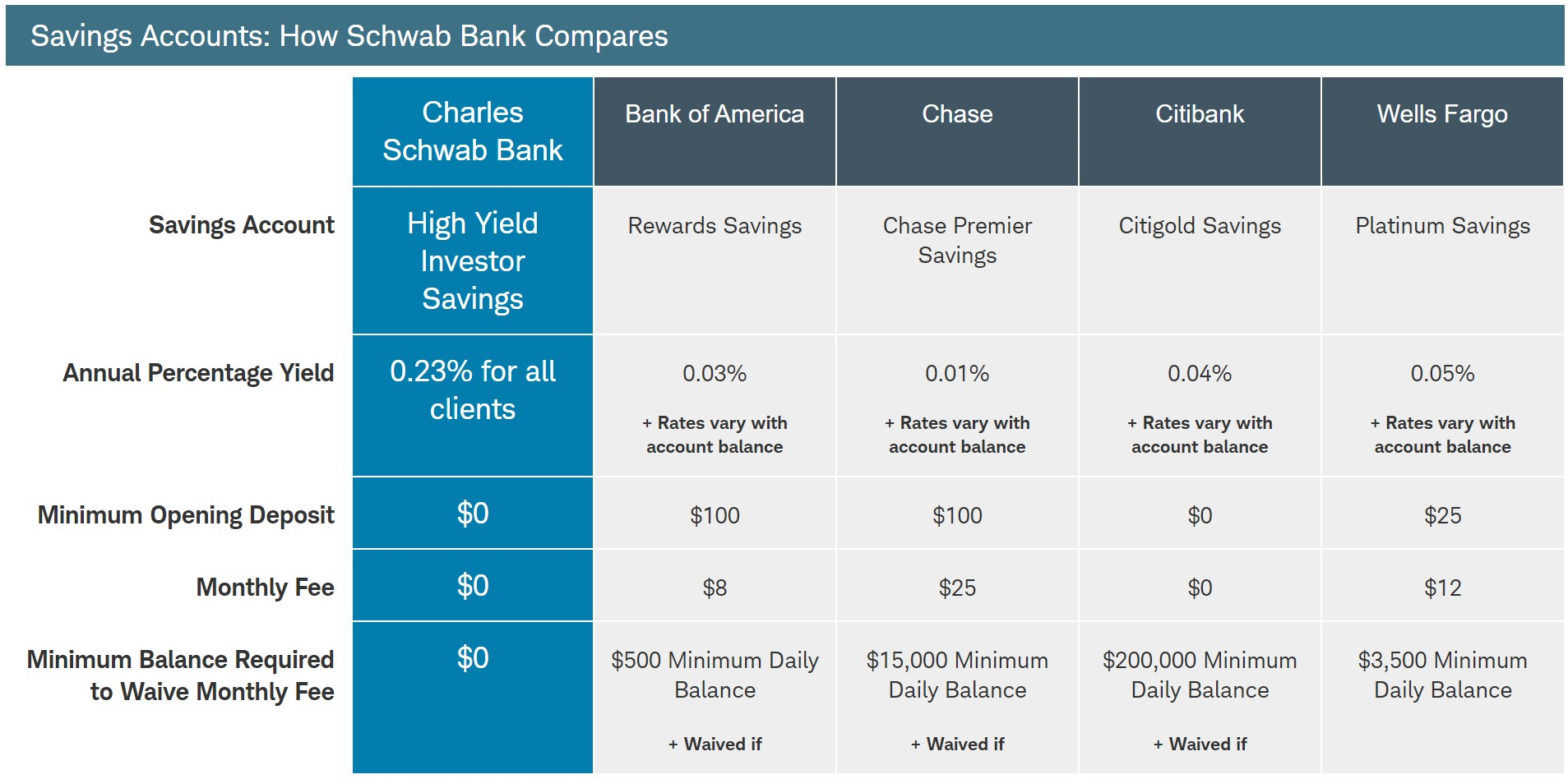

Before I got my HYSA, I had all of my cash in a Schwab “High Yield Investor Savings” account. Despite the words “High Yield” and “Savings” in the name, I was only earning a 0.23% interest rate – and even then, I was doing exceptionally well. The Schwab account outperformed many competing offerings from other banks (chances are, if you don’t use an HYSA, it’ll beat yours too):

But the Schwab account wasn’t a real HYSA. Real HYSAs, in my mind, have 2 defining features:

They’re earning an interest rate that’s about where the federal funds rate is.

They’re insured by the FDIC.

Understanding what the “federal funds rate” is isn’t important. What is important is that right now, most HYSAs are earning around the neighborhood of 1.90% interest, roughly 8x what I was earning previously. Put another way, for each $10,000 I had saved up, I’d be earning $157 more per year in interest, or a Netflix subscription – HYSAs are free Netflix (This one weird trick saved him hundreds! Netflix hates him!). If you have money saved up, you should find out what interest rate you’re earning on that cash, and compare it to the HYSA rates available.

What’s a FDIC?

Essentially, the FDIC-insured label means that if you have a savings account with money in it and the bank holding that money goes bankrupt, you won’t lose your money. The FDIC is a government corporation, so everything’s fine unless the US government starts to have issues (and at that point, you’ve got bigger problems). This only applies to FDIC-insured accounts. While companies (e.g. Schwab) offer “money-market funds” that can earn an interest rate around the neighborhood of HYSAs, money-market funds aren’t FDIC-insured, which means that you lose one layer of insurance in case another Great Depression happens.

Inflation, and why it’s less Free Money and more Not Burning Money

Intuitively, we all know about inflation. It’s why Subway doesn’t have a $5 footlong any more, why the dollar menu at fast-food joints has been steadily replaced with a “value menu”, and why you remember things being cheaper across the board when you were younger. Prices steadily increase over time for most things, and that’s just the way the world works. So, while an HYSA probably won’t beat inflation (at least, it doesn’t today), it’ll at least beat a standard savings account, where your money will just stagnate. With a standard low-yield savings account, you won’t see any noticeable gains on your money at all, which means you won’t be building up a buffer against inflation. With an HYSA, at least your interest earned will partially offset what inflation eats away at.

What’s all of this for?

HYSAs are a great place to store liquid cash that you need to hold its value. While you’re investing your retirement, you want money to grow, and you don’t really need the liquidity, so you probably shouldn’t be using an HYSA to invest for retirement. There are two categories of things I can think of where an HYSA makes sense:

To hold your emergency fund.

To hold cash for a purchase you’re about to make soon that you don’t want to be subject to market volatility.

There also might be something that I’m missing. On the first point, there are stories on stories on stories on stories of why you need an emergency fund – and an HYSA is a great place to keep it. On the second point, if you’re about to buy a new laptop, car, or some other relatively-large purchase, you’ll want to sleep well at night by not worrying on whether you can afford it or not. Markets go up and down on a daily basis. Investments can be volatile. Money in the bank, however, shouldn’t be – and that’s where the HYSA comes in.

Some Options I Found

Like my last post, I wanted to specifically call-out some of the options I’ve seen throughout my research. For full transparency, I’ve only recently moved my money into an HYSA, so my total experience is about a couple of days at this point. Nevertheless, hopefully the following shortlist will be helpful.

Marcus

Marcus is a new arm of Goldman Sachs that’s focused on normal-people instead of Goldman’s normal clients. I ended up personally going with Marcus as my HYSA, and I can’t say I have any complaints here. At the current time, I’m earning 1.9% on my money, and I generally like the web interface (there’s no apps for Android). Customer support is available 7 days a week, though not 24/7. There’s no debit card you can get, nor are there any ATMs you can use to access your money. You also can’t easily deposit checks, due to the lack of a mobile app. With all of those caveats in mind, I’d note that, for most people, none of them will really matter.

American Express Personal Savings

American Express, in addition to their credit products, also has a Personal Savings arm that more or less does the exact same thing as Marcus – same interest rate, same limitations, same lack of fees and minimum balance requirements (while there’s an American Express app, there’s no way to access the Personal Savings side of things, as far as I know). I’ve heard that the web interface isn’t as nice, but Amex’s support is available 24/7, and at least on their credit cards, it’s phenomenal.

Ally Bank

Ally is often recommended on Reddit, as it (like Marcus and Amex) has no fees, a competitive rate, and solid 24/7 support. Right now, they’re paying 1.80%, though you shouldn’t worry about the 0.1% difference too much. Unlike Marcus and Amex, they do have a mobile app with a check-deposit feature, and they’ll also allow you to use out-of-network ATMs. Ally is a bit of a curious case, since user reviews online are mostly-negative, though everyone on the Personal Finance subreddit seems incredibly happy.

You Don’t Need to Chase Partial Percents

In the grand scheme of things, it probably isn’t all that important to chase tenths or hundredths of a percent when you look for an HYSA. A 0.1% difference translates to less than a dollar per month per $10,000, so it’s unlikely that it’s really going to be worth your time to chase the highest rate.

Rates will change periodically, both up and down, to adjust to what the government sets as the federal funds rate. It’s not worth moving your money around from one bank to another just to earn a few extra hundredths of a percent – as long as your bank is fairly competitive and you like the support, there’s probably not much of a reason to worry.

Never Pay Fees, Don’t Accept Minimums

This is quite simple, really – just don’t pay fees. If a bank is charging you to hold onto your money, whether through transfer fees, monthly fees, or monthly minimums (requiring you to keep a certain amount of money in the account for it to be valid), you should probably look for another bank. Fees eat away at your interest, which means you’re effectively earning a lower rate than you should be. Citibank, for example, requires a balance of $500 to avoid getting hit with a monthly fee.

Some Other Resources

As always, the personal finance subreddit is a wonderful place to start. They’ve also compiled a helpful list of banks and credit unions they recommend.

Update: A friend told me that I left out Robinhood Cash Management, which is FDIC-insured and is currently advertising a 2.05% interest rate. While things look good on paper, it’s not an actual product yet (at the time of writing), so I didn’t include it on my shortlist. Nevertheless, it could be pretty interesting.